By

Jim Hingst

Jim Hingst is a contributing writer for Sign Builder Illustrated magazine.

Choosing

the right business structure is an important first step when starting a

company. It affects your taxes, your exposure to liability and your

relationship with partners. In the case of corporations, it also affects the

amount of paperwork you are required to fill out.

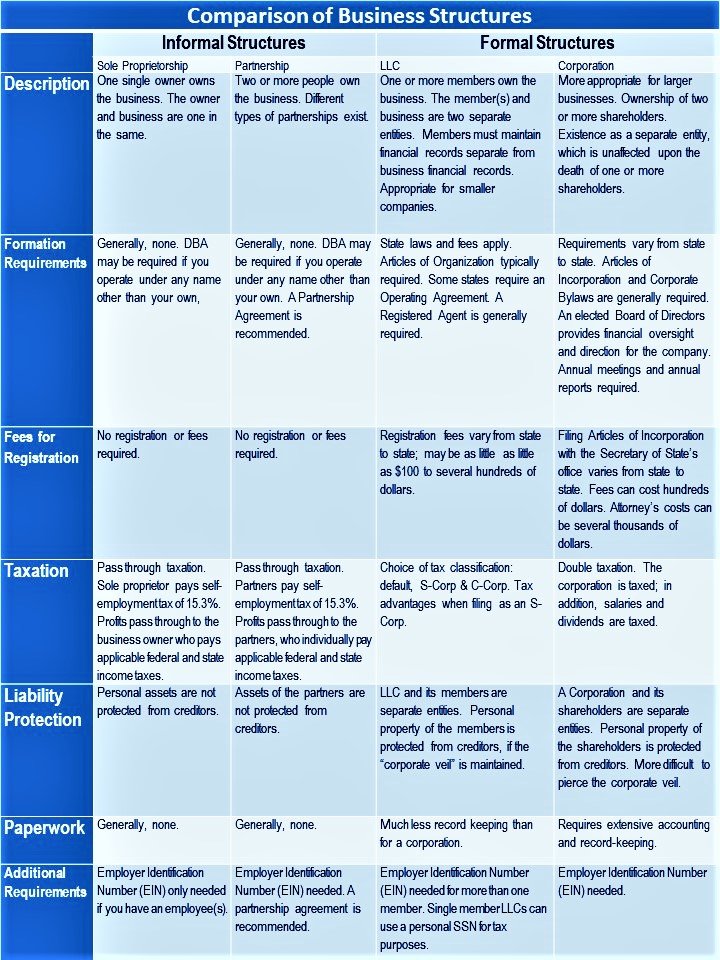

Business

structures fall into four basic categories: Sole Proprietorship; Partnership;

Limited Liability Company (LLC); and Corporation. Both sole proprietorships and

partnerships are designated as informal business structures. Both are

“pass-through entities” which means that the profits pass through the business

to the individuals. Rather than taxing the business for their profits and then

taxing the individuals on their wages from the business, sole proprietors and

partners only pay taxes once on their personal tax returns.

LLCs

and corporations on the other hand are classified as formal business

structures. That means that these structures exist legally separately from

their owners. It also means that these businesses are subject to state and

federal regulations in order to preserve their legal status.

Formal

business structures, such as an LLC or Corporation, protect your personal

assets in the event that you are sued or default on a loan. A formal structure

also imbues your company with an aura of credibility.

Is

a Lawyer Necessary?

You

don’t need a lawyer to set up an LLC or a corporation. If you have all the time

in the world, you can research the particulars involved in setting up your

business and filing. Filing can easily be done on-line.

The

reason that you should have a lawyer is that they are professionals. It’s what

they do for a living. They have the experience to do things the right way and

to do the job quickly. If you don’t do things the right way, you may need a

lawyer at some time in the future if you mess things up. It’s your decision:

pay the lawyer now or pay him later.

One

important area where an attorney can help you is in deciding on LLC taxation.

Do you want to be taxed as (1) sole proprietorship or partnership; (2) an S-Corporation;

or (3) a C-Corporation?

Generally,

taxation as a C-Corp for a small business is unrealistic. Large organizations

may select this option if you intend to reinvest a significant portion of your

profits in equipment or property or you have many investors. The disadvantage

of a C-Corp is double taxation. The

corporation is taxed and then you as an owner and your employees are taxed.

If

you are starting a new company, before you decide on your business structure

(i.e., sole proprietorship, LLC, corporation) first consult your attorney and

CPA. The legal structure that you select will impact your personal liability

and affect how you will be taxed.

In assisting

you in choosing the right structure for your business, an attorney can help you

avoid potential liability exposure. He can also help in obtaining any necessary

business permits. What’s more, by reviewing and analyzing all of the different

types of contracts you are involved in, such as leases and contracts with your

business partners, he can protect your interests.

Sole Proprietorship.

As a

sole proprietor, you are “the king of me.”

You and your business are one and the same. It is the easiest way to

start a business. That can be a good thing, but at other times, not so good.

You rake in all of the profits, but you are on the hook for all of the debts.

What’s worse, you are personally liable if you default on a loan or are sued.

The good news is that if you open your

shop as the only owner, you are a sole proprietor. You will, however, need to

obtain any applicable state and local licenses and permits. You may also be

required to file for a DBA with your County recorder if you operate your shop

under any name other than yours.

Starting a sole proprietorship is easy

and inexpensive. Compared to other business entities, taxes are lower. What’s more, you are your own boss with no

one to answer to. There are some downsides. You are personally responsible for

all of your business liabilities. As a sole proprietor, you may also have more

difficulty getting a commercial loan.

Running your shop as a sole proprietorship provides you

with many advantages that other business structures do not have. You have fewer

government regulations. Your tax obligations may also be lower because you are

only taxed at the personal level. However, as a sole proprietorship you are

self-employed and incur the self-employment tax of 15.3% along with applicable

federal and state income taxes.

The catch is that you are personally liable for all of

your shop’s debt. What’s more, if your business is sued and a judgement goes

against your company, you are personally liable. That means that you could lose

your home or other assets.

A

general rule of thumb, if you are starting out in business or your shop is

earning less than $40,000, you should operate your business as a sole

proprietorship.

If

you have significant personal assets, you should form an LLC before you start

your business to protect these assets.

A

single member LLC is taxed as a sole proprietorship and incurs the full 15.3% self-employment

tax.

More

than half of the businesses in the U.S. are sole proprietorships. You don’t

need much more to get started than the tools of your trade. If you don’t employ

anyone, you don’t need an Employer Identification Number (EIN). You don’t even

need a separate business bank account. In fact, you will unlikely get a

business account without an EIN. You simply file taxes using a Schedule C tax

form.

The

problem that sole proprietorships face is that because the line between

personal expenses and business expenses is often blurred, the IRS is more

likely to audit you versus operating as a more formal business structure. When

you face an audit, there is a high probability that you will lose and end up

paying more in taxes and penalties.

If

that isn’t bad enough, as a sole proprietorship it is easy for someone to sue

you. That puts all of your personal assets at risk. That may not bother you in

the first place if you are dirt poor and have nothing to lose. However, a

tenacious and vindictive litigant can pursue you to the ends of the earth to

your dying day. Even after you lose everything you own, he can garnish your

wages.

In

the event that you pass away, as a sole proprietorship your business dies with

you. That can be a problem for your family if they want to sell the business.

It

is also more difficult for a sole proprietorship to obtain a business loan than

operating your business using a more formal business structure, such as an LLC.

General Partnership.

At the very least, when forming a

partnership, you should have a written partnership agreement. Never form a

partnership on a handshake even when the partner is a friend or a family

member.

A partnership agreement is a contract

between you and your business partners. The value of a partnership agreement is

that it avoids possible disputes. When it comes to money, disputes are common.

What’s more, as the saying goes, there is no such thing as friends when it

comes to money.

Some areas that a detailed written

agreement should include are:

• The nature of your business.

• Capital contributions of each partner.

• Distribution of profits and losses.

• How members withdraw from the

partnership.

• Dissolution of the partnership.

A lawyer can help you structure an

agreement and address all of the possible pitfalls that you can encounter when

going into business with someone else. The fact is that partnerships rarely

work for a variety of reasons.

A

better alternative to a general partnership is a multi-member LLC. This

business structure not only delivers all of the benefits of a formal general

partnership agreement, but it also provides personal asset protection and

flexibility in how your company is taxed.

Limited

Liability Company (LLC).

Among

small businesses, an LLC is the most popular business entity. Not only does it

protect your personal assets, it also provides tax benefits, such as

pass-through taxation. When profits pass directly through to the owners, the

owners, not the business, are taxed. By comparison, businesses which are set up

as C-corporations are taxed twice. First, the profits that the company makes

are taxed. Then anything paid to the members is taxed again. Of course, an LLC can

choose to be taxed as a C-corporation, which makes no sense for most

businesses.

Tax

Benefits of an LLC.

You can

realize tax benefits as the sole member of an LLC, if you select to be taxed as

an S-Corp. Here’s how. If your shop makes a profit of $100,000, you can pay

yourself half as wages and half as dividends. If all of the profits are passed

through to your personal tax statement, the normal self-employment tax is about

$15,000. The self-employment tax of 15.3% covers 12.4% for Social Security and

2.9% for Medicare. You must also pay federal and state income tax.

On the other

hand, as an S-Corp, if you pay yourself a reasonable salary of $50,000, you can

reduce the self-employment tax by 50%. If this sounds like bookkeeping

finagling, keep in mind that the IRS is more likely to audit you when filing as

an S-Corp. For this reason, you should consult a lawyer or a CPA when selecting

how your LLC should be taxed. If the IRS

deems that $50,000 is not a reasonable salary and some of what you paid

yourself as dividends should be reclassified as wages, you could face tax

penalties.

LLCs with

multiple shareholders are not that different from a single owner LLC. When an owner of an LLC filing as an S-Corp

performs tasks within the business, he must be treated as an employee. He must

receive reasonable compensation for his work. In addition to payroll deductions

for Social Security and Medicare, federal and state taxes must also be

withheld. With respect to other employees, the owner must contribute half of

their employment taxes and all of his own. In part tax savings are realized

from the money paid to shareholders, which is not subject to employment taxes.

Another tax benefit is that unlike a C-Corp, LLCs and S-Corps do not incur

corporate taxes, because they are pass-through entities.

Single Member

LLC. If you are a

one-man shop, set up as an LLC, you can segregate business finances from

personal finances. This permits you to write off business-related expenses,

such as office supplies and travel and entertainment costs.

For tax

purposes, you may need to file any number of tax forms that were not required

when filing as a sole proprietor. This can be complicated. For this reason,

consult your CPA or tax professional.

What is a Reasonable Salary?

Taxed as an S-Corp, you must pay yourself a “reasonable

salary” commensurate with the salary that you would pay someone to do your job.

If the IRS scrutinizes your tax return and

deems that you are not paying yourself a reasonable salary, you can be subject

to additional tax and penalties. What’s more, you could lose your S-Corp tax

filing status.

Generally, if your excess earnings exceed

$10,000 to $15,000 after paying yourself a reasonable salary, then electing

S-Corp tax status probably makes sense. Keep in mind that you can always change

your filing status on the future tax returns.

S-Corp status makes sense if you plan to take

the excess earnings as a distribution. On the other hand, if you plan to

reinvest these earnings at a later date, you might be better off selecting the

C-Corp tax status.

Disadvantages of S-Corps.

To run payroll, you will need a bookkeeper.

That cost may be significantly higher than any tax savings you may realize.

Choosing

a Tax Classification. As an LLC you have the choice of tax

classification. These choices are default, S-Corp and C-Corp. The default tax

strategy is pass-through taxation. If

you are the sole member in an LLC, you are taxed as sole proprietor. When an

LLC has multiple members, your business is taxed as a partnership. That means

that profits are distributed among the members and subject to employment taxes.

An S-Corp

is a little more complicated. Members can receive a salary and receive

distribution of profits. If you choose this tax classification, your accounting

will be more complicated and you will probably need professional assistance in

accounting and tax preparation. As a word of caution, the IRS more thoroughly

scrutinizes tax returns for S-Corps compared to tax classifications as sole

proprietorships and partnerships.

Articles

of Organization.

One

of the usual requirements is submission of “articles of organization”, also

known as the certificate of formation. The Articles of Organization provide a

basic overview of the LLC that you are forming. This information includes the

name and address of the business, the name and address of your registered

agent, the purpose of your business and its management structure. This process

also requires a filing fee, which may cost as much as $200.

Your Operating Agreement.

In

registering your business, you should have an operating agreement, whether your

state requires it or not, and whether the company is a single-member LLC or a

partnership LLC. This agreement describes the rules under which your business

will be run.

An

operating agreement is a contract that governs the economic relationship among

members. It describes the operation of the LLC, such as who makes decisions,

the rights and responsibilities of members, resolution of disputes,

distribution of profits and admission of new members. Without an operating

agreement, the state’s default rules serve as a guideline for the LLC. The

agreement prevents litigation in the event of disputes.

As

a foundation, the operating agreement allows the members to indicate the

initial investment each made and stipulate the percentage of ownership. It also

specifies the tax classification for the LLC. Members can decide whether the

LLC should be taxed as a sole proprietorship, partnership, S-Corporation or

C-Corporation. The agreement also allows members to stipulate how to handle the

community property interests of spouses, if you are in a community property

state.

While

your state may not require an operating agreement when filing for an LLC, you

may need one when applying for a bank loan. An operating agreement also is

helpful in court when investigating liability. In other words, the court may

decide whether to assign liability to either the LLC liable or to the members.

If a single-member LLC decides that it is

not to be treated as a corporation for tax purposes, it falls into the

classification of a “disregarded entity.” In this classification, the business

is considered to be separate from its owner for any liability. However, for tax

purposes, profits pass through the business to the owner. The owner pays income tax on the company

profits on his or her personal income tax return.

In many cases, if your single-member LLC

is classified as a disregarded entity, you can simply use your social security

number on your federal tax return. However, if you have employees, you will

need an Employer Identification Number (EIN). You are generally better off

getting an EIN.

Other

than California, Delaware, Maine, Missouri, Nebraska and New York, you are not

required to adopt an operating agreement. What’s more, no state requires that

you file one with the Secretary of State, where the LLC was formed.

Nevertheless, you should create an operating agreement for your business, even

if your company is a single-member LLC. Here’s why you need one:

•

An operating agreement establishes guidelines for resolving any legal disputes

that may arise. Without one, the LLC must follow your state’s default rules.

•

Banks and other lenders may request an operating agreement when you open a

business bank account or apply for a loan. The operating agreement ensures the

lender that the person acting on behalf of your company has that authority.

•

If your business is a single-member LLC, an operating agreement helps safeguard

your company’s limited liability standing.

What

an Operating Agreement Entails. In

structuring an operating agreement, include the following components:

•

Basic company information: Business name, location, purpose, duration of the

LLC;

•

Names of the members (owners);

•

Explanation of how members are compensated (salaries and distribution of

profits);

•

Voting rights of the members;

•

Contact information for your registered agent. When you start an LLC or

corporation, you must designate a registered agent (also known as a resident

agent or statuary agent). The registered agent is authorized to represent your

company. He or she is your point person, who receives government notices,

documents and other correspondence. Your

operating agreement must list the agent’s physical street address and other

contact information. The registered agent must also be available during normal

business hours;

•

Designate whether your LLC is member-managed or manager-managed. The difference

is that in a member-managed LLC, the members or owners run the day-to-day

operations. In manager-managed LLCs, the members hire managers to run the

company.

•

Define the responsibilities of the members and managers;

•

Indicate how the LLC elects to be taxed;

•

Procedure for adding and removing members; and

• Explain

the process for dissolving the LLC.

The

members should sign the operating agreement and stored it with your other

business documents. Each member should receive a copy.

Employer Identification Number.

If you have employees or your business is

organized as a partnership, LLC or corporation,

you will need an Employer Identification Number (EIN), also known as a federal

tax ID number.

Every formal business structure must

apply for an EIN from the IRS, after (not before) your business is

legally formed. You also must apply for an EIN if you hire an employee even as

a sole propitiator or partnership or private individual. The application

process is simple. While you can apply by mail using the IRS Form SS-4, it is

much simpler to apply on-line.

The EIN is the

equivalent of a social security number for your company. You will need an EIN

to file your state and federal tax returns, apply for business licenses, open a

business bank account, hire employees or withhold employment taxes.

Employment Taxes. As an employer you must

withhold federal and state income taxes from the wages of your employees. You

must also withhold Social Security and Medicare taxes. Employees pay half of

the FICA taxes and as an employer you must contribute half of their taxes. That

amount to 6.2% for Social Security and 1.45% for Medicare of your employees’

wages. What’s more, you must also pay for Federal Unemployment tax out of your

company funds, not from your employees’ wages.

Choosing a Registered Agent.

When

you file for an LLC or form a corporation, you will generally be required to

designate one person as a “Registered Agent” also known as a statutory agent.

This is the person assigned to receive time-sensitive legal documents, such as

subpoenas, lawsuits or tax notices, for your business. The registered agent

then forwards the documents to the appropriate person within your company. The

person assigned must have a physical address. The registered agent can be a

member of the LLC or you can hire a service.

Not having a registered agent can result

in serious legal problems. If a process server cannot contact your registered

agent, the court can continue with the case and rule against your company

without you even being aware. Failure to maintain a registered agent can result

in the state fining your company and even in dissolution of your LLC or

corporation. When this happens, you could lose the liability protection that

your LLC or corporation provides and you put your personal assets at risk.

Do You

Need a DBA?

The DBA

(doing business as) permits a company to operate using a name or brand which is

different from the legal name of the business. You should contact the business

services division of your Secretary of State’s office to learn what is required

in your state. How and where you file can vary depending on your company’s

business structure. Generally, the DBA requirement is satisfied as part of an

LLC application.

A DBA

does not provide you with any legal protection for your business names or

brands as a trademark would. A DBA is also no substitute for an LLC and does

not protect your personal assets. It is simply a state legal requirement.

The Corporate Veil.

A key

reason to form an LLC or corporation is to provide yourself a “corporate veil”

which protects your personal assets, such as your home, cars and savings. The

corporate veil, however, is not bulletproof if creditors or plaintiffs have

sufficient grounds to pierce the veil. These grounds include fraud,

insufficient funding, inadequate insurance coverage or failure to follow

corporate formalities. Plaintiffs can also appeal to the court’s sense of

fairness in lieu of other grounds. The protection of the corporate veil varies

from state to state.

Preserving the Corporate Veil Protection. Just as C-Corps and S-Corps have corporate veil protection so do

LLCs if you follow the necessary procedures. This veil must be maintained or

you lose its protection. To prevent this from happening you should take the

following steps:

• Create

and maintain an operating agreement, resolutions, bylaws and annual owner’s

meeting minutes and membership certificates.

• Make

sure that the company owns all of the equipment, tools, vehicles and supplies

used at your business.

• Keep all

funds for the LLC separate from the personal funds of the members. In addition,

open a bank account for the LLC and apply for a business credit card. In

setting these up, you should use your EIN number not your social

security number.

• When you

buy anything, sign contracts or write company documents make sure that you do

it in the company’s name not your name. Make sure you establish your LLC before

you purchase any business assets. This can help avoid any issues when

transferring title of property under your name to the LLC. As a condition of

your mortgage, you may be required to pay off the mortgage before title

transfer.

•

Publicize the existence of your LLC on your website, social media, news

releases and marketing literature.

Business Insurance.

An LLC

helps protect your personal assets. It does not, however, protect the assets

that the business owns. In most cases, liability insurance is the most

important coverage that your business needs. It covers your company for any

claims against your company. You should also consider investing in commercial

property insurance, a policy for company vehicles and business interruption

insurance. Of course, you will also need worker’s compensation insurance to

comply with your state’s requirements.

A

commercial umbrella insurance policy protects your business for any claims that

are beyond the coverage of your other policies. It is not a substitute for your

regular insurance policies.

Melissa Cox of Snyder Insurance

Agency Inc. in Michigan City, Indiana advises that you should sit down with an

insurance professional ensuring that the policy is written correctly based on

the business entity type you choose. With a sole proprietorship operating with

a DBA, the insurance policy should name both you as the owner and the business

name. Consider your liability limit carefully. If your business is sued

for more than your insurance limit, it will be paid out of business assets. In

the case of a sole-proprietorship or partnership, it will come out of the

owners’ pockets.

Cox also says that if you will have employees, it’s also a good

idea to talk to an agent about how worker’s compensation will be handled. Worker’s

Comp is different for an LLC and Corporation than it is for a sole

proprietorship. The Owners may or may not be covered and could be subject to a

minimum payroll rating, directly affecting the premium.

Selecting

S-Corp Tax Classification.

An

S-Corp is a tax classification you can select if your business structure is an

LLC. It is not a formal business entity like LLCs and C-Corporations. If

you decide to classify your business as an S-Corp, be prepared to do more

paperwork.

When

you elect the S-Corp tax classification, you can realize significant savings on

your taxes. As a member of an LLC you are not an employee of your company. You

are an owner. As an owner you can pay yourself a salary as an employee and

receive a distribution of profits. Each type of payment is taxed differently.

By

comparison, if you elect to be taxed as either a sole proprietorship or as a

partnership, all earnings pass through to the members. All of these earnings

are subject to employment tax and federal and state income taxes.

Certain

restrictions apply to S-Corps. These include:

•

Having fewer than 100 employees.

•

Owners must be U.S. citizens or legal residents.

•

Individual members must not include LLCs or Corporations.

•

S-Corps can only issue one class of stock.

Protecting LLC Assets in a Revocable Living Trust.

Putting all of the assets of your LLC into a revocable

trust has many benefits. To protect your company’s assets for your

beneficiaries, a revocable living trust can have either sole or partial

ownership of your LLC. A revocable trust is a living trust which allows the

person who formed it to change or revoke it at any time.

One advantage of having a revocable living trust own

all of the LLC membership assets is to name a successor trustee to administer

the affairs of your company in event you become incapacitated.

In the event that you would pass away, the company

assets would be held in trust, which would avoid probate. The assets can be

either distributed at the time of death of the owner or the administrator can

continue to manage the business.

To avoid any confusion, your trust document should

include all of the details covering the management of the business. In the case

of dissolution of the business, an estate distribution plan will ensure that

the assets of the trust are divided among your beneficiaries in the way you

want. This also protects the estate against claims of creditors and ex-wives.

Putting your LLC into a revocable living trust is a

conversation that you should have with your attorney at the time you discuss

the topic of business structures.

Forming a

Corporation.

The requirements for forming a corporation are governed by the

rules in the state where the business is formed. Generally, you should

incorporate in the state where your company operates. You may have heard that

some businesses incorporate in Delaware and Nevada because their laws are more

business-friendly. While this is true, you must also register your company as a

foreign corporation and pay taxes in the state where it is physically located

and operating. In addition, you also must pay taxes in Delaware or Nevada.

Forming a

corporation makes sense if your company has more than 100 employees and generates

significant sales and profits. The

C-Corporation establishes a business as a separate legal entity. In other

words, the company exists independently or separately from its owners or

shareholders.

For a larger

corporation, this business structure has advantages. The biggest advantage is

limited liability. Another advantage is stability. Because a corporation is a

separate legal entity, if one of the owners dies, the business continues. A

sole proprietorship or partnership frequently dies when an owner dies.

For a smaller

company, forming a corporation requires time-consuming paperwork and more

expense. Double taxation is another disadvantage. Because a corporation is not

a viable business structure for most small companies, this article will not

devote much time to it.

Articles of

Incorporation.

One of the

first tasks required in forming a corporation is to write Articles of

Incorporation. These are similar

to Articles of Organization required for LLCs. The requirements will vary from

state to state. You will need to inquire about these requirements at the

Secretary of State’s office for your state. Generally, they will have forms and

guidelines covering the preparation of these articles.

The Articles of Incorporation

provide the basic information and outline for the business including company

name and location; names of the members on the board of directors and the

numbers of shares which can be issued.

Corporate Bylaws.

While the Articles

of Incorporation provide a basic outline of the business, the Corporate Bylaws

get into the specific rules governing the organization. These specifics might

outline the company mission and objectives; responsibilities of each of the board

members; how meetings are conducted; how the board of directors are elected and

how they in-turn select corporate officers.

While you can

write your own Articles of Incorporation and Corporate Bylaws the easiest way

to prepare these is to consult with your attorney.

Conclusion.

For most

companies, forming your company as an LLC is your best option. Whatever choice

you make, make sure to take the following steps:

• Do your

homework. Read as much as you can about the advantages and disadvantages of the

various business structures.

• As part of your

research, contact your Secretary of State’s office. Find out the regulations,

forms and procedures necessary to form a business in your state.

• Discuss the

different business structure options with your attorney and CPA or tax professional.

• Do all of your

planning before you open for business. Remember that proper prior

planning prevents poor performance.

© 2022 Jim Hingst, All Rights Reserved

{kind=link}